This core principle of finance holds that, provided money can earn interest, any amount of money is worth more the sooner it is received.

Factors affecting time value of money:

- The nominal risk-free rate of return

- Inflation

- Risk

Future value(FV)

If a capital amount is invested today, it will offer interest in future periods.

Type of interest:

- Simple interest

It is money you can earn by initially investing some money (the principal). A percentage (the interest) of the principal is added to the principal, making your initial investment grow.

- Formula: FV = Pv(1 + r n)

- Compound interest

Compound interest is interest added to the principal of a deposit or loan so that the added interest also earns interest from then on. This addition of interest to the principal is called compounding.

- Formula: FV = Pv(1 + r)ⁿ

Present value(PV)

When the future value and interest rates are known, the present value of interest may be determined through discounting.

- Formula: PV = Fv/(1 + r)ⁿ

Effective Annual Rate

Effective Annual Interest Rate is an investment's annual rate of interest when compounding occurs more often than once a year.

Example:

An investment of Rs 1000 is made at a 6-monthly interest rate of 5%. The interests are compounded on a 6-monthly basis over 3 years.

Annuity

An annuity is a series of equal payments at regular intervals. Examples of annuities are regular deposits to a savings account, monthly home mortgage payments, monthly insurance payments and pension payments.

An ordinary annuity is a series of equal payments made at the end of each period over a fixed amount of time.

Formula:

An due annuity is a repeating payment that is made at the beginning of each period.

Formula:

Effective Annual Interest Rate is an investment's annual rate of interest when compounding occurs more often than once a year.

Example:

An investment of Rs 1000 is made at a 6-monthly interest rate of 5%. The interests are compounded on a 6-monthly basis over 3 years.

Annuity

An annuity is a series of equal payments at regular intervals. Examples of annuities are regular deposits to a savings account, monthly home mortgage payments, monthly insurance payments and pension payments.

An ordinary annuity is a series of equal payments made at the end of each period over a fixed amount of time.

Formula:

An due annuity is a repeating payment that is made at the beginning of each period.

Formula:

Questions:

- A project has cash flows of

$15,000, $10,000, and $5,000 in 1, 2, and 3 years, respectively. If the prevailing

interest rate is 15%, would you buy the project if it costs $25,000?

- Suppose

you deposit $1,000 today in an account that pays 5% interest at the end of each

year. If you withdraw one half of the yearʹs interest at the end of each year,

what is the balance in your account after your third withdrawal?

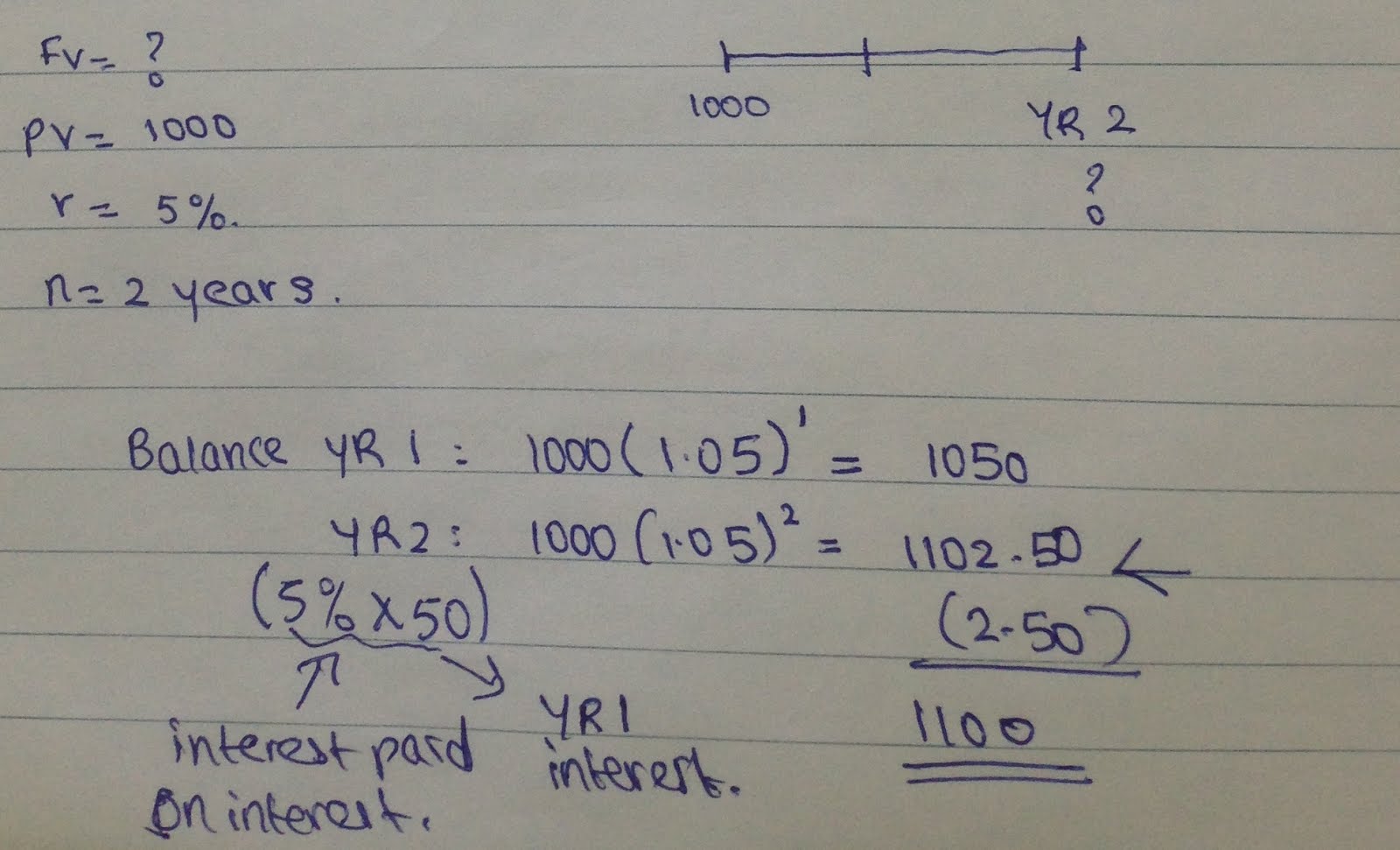

- Suppose

you deposit $1,000 today in an account that pays interest at an annual rate of

5%. What will be the balance in the account at the end of two years if you

withdraw only the interest paid on the interest at that time?

- Which

is the better deal: a deposit of one penny today in an account that will offer

a daily return of 100% for one month (i.e., the value of the account is doubled

every day for 30 days) or a lump sum of $10 million to be received thirty days

from today?

- Three

years ago, Karen deposited $25,000 in an account that paid 8% annually. Today,

she transferred the funds in that account to an account that will pay her 10%

annually. How much will she have in her account three years from now?

- Maria has decided that she can

live on $80,000 a year upon retirement, and she expects to live for thirty

years after she has retired. If she can earn an average annual rate of return

of 8% after she retires, what minimum amount must she have accumulated in her

retirement account one year before she makes her first withdrawal in order to

meet her requirement?

- Freedom

Enterprises is considering investing in a project that is expected to produce $12,000

in cash flows each year for five years. If Freedom Enterprisesʹ cost of capital

is 14%, what is the maximum the firm should be willing to invest in this

project? Assume the first cash flow will occur one year after the investment is

made.

- An

insurance agent has recommended you invest in a policy that promises to pay you

$10,000 a year upon retirement. The payments will continue for 15 years after

you retire. If you plan to retire in 25 years and can earn a constant effective

annual rate of 12% on similar investments, what is the maximum you should be

willing to pay for this policy today? Assume the first payment will be made at

the end of the 25th year.

I really like this article please keep it up.

ReplyDeletewill help you more:

N26 to niemiecki bank dostępny w Polsce, czyli darmowe konto z kartą bonusem 15 eur. To jedyny bank ktory umozliwia otwarcie konta w Niemczech dla osób, które na codzien mieszkają w Polsce. Sprawdz rowniez opinie o n26.

n26 opinie